Testing

What we learned from research.

Giving existing Business Banking customers a digital way to update their contact details and marketing preferences — replacing a broken offline process and unlocking a significant data gap for the bank.

"If I want to update my email address, I either fill in a paper form or call them. So I just don't bother."

Lloyds Business Banking had a significant data problem: contact information for a large proportion of existing customers was either missing, incomplete, or years out of date. There was no self-serve digital way for business customers to update their contact details — if they wanted to make a change, they had to call customer service or complete a paper form.

Predictably, most didn't bother. The result was a growing gap between the customers the bank thought it could reach and the ones it actually could — with real consequences for regulatory communications, fraud alerts, and marketing reach across the business banking portfolio.

Beyond the data quality issue, the bank also lacked structured marketing consent from many of its business customers — limiting its ability to communicate relevant products and services to the businesses it served. The opportunity was clear: build a digital journey that fixed the data gap and collected meaningful opt-ins at the same time.

Behaviours we were driving

Behaviours we were discouraging

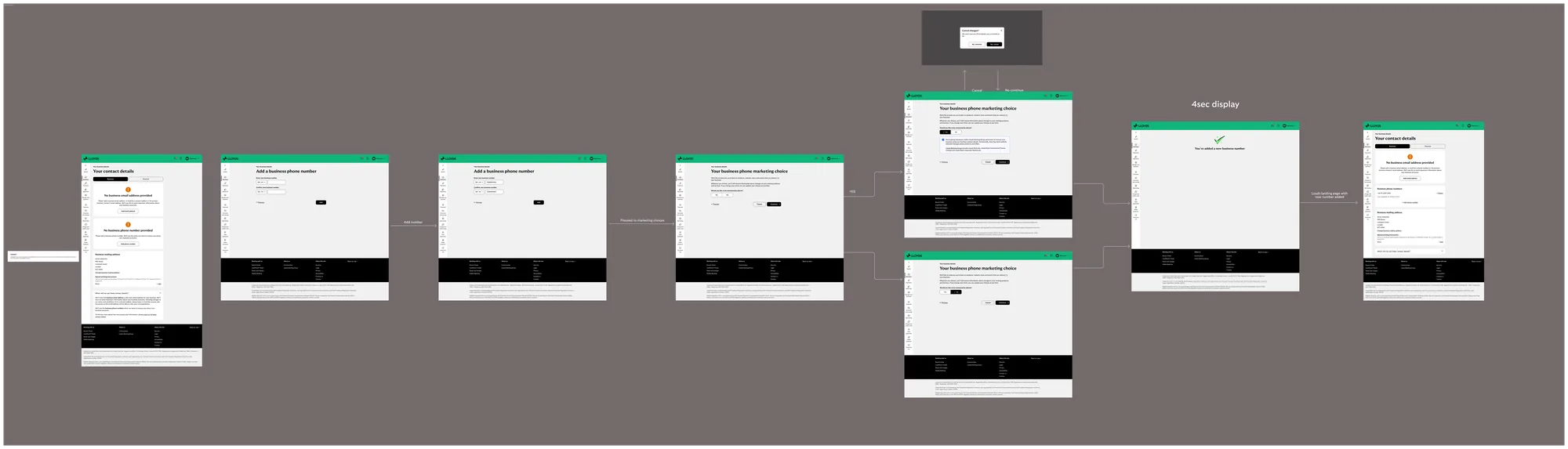

We decomposed the form into a one-question-at-a-time flow, logically sequenced to mirror how customers actually think about their contact information — personal details first, then communication preferences, then marketing choices. Each screen focused on a single decision, with clear labelling of what was required and what was optional.

Rather than burying marketing consent in regulatory language, we redesigned it as an explicit, honest offer. Plain-language descriptions explained what each channel would be used for, with specific examples. We gave customers granular control — by channel, not just a blanket yes/no — and made it clear they could change their mind at any time. Testing showed this approach increased opt-in rates while improving customer trust scores.

We worked with legal and compliance teams from the start of the project — not as a final review gate. This allowed us to find design solutions that met FCA requirements without sacrificing clarity. Where compliance required specific language, we isolated it in expandable detail sections rather than surfacing it as the primary content. Everything was signed off by legal before entering the design system.

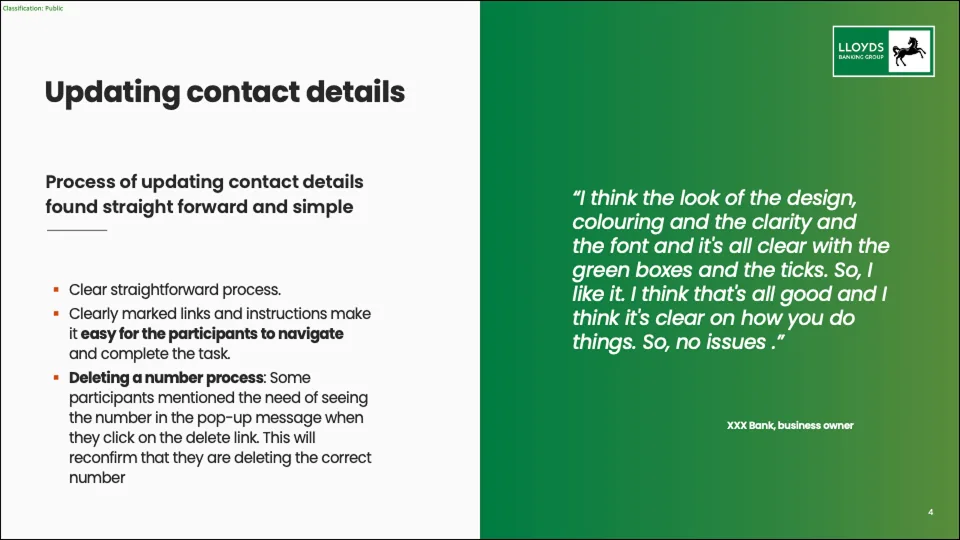

For returning customers in periodic review journeys, we pre-populated fields with known information and surfaced only what had changed or needed reconfirmation. This dramatically reduced the perceived effort of the journey — customers who had completed it before reported that it felt "completely different" and "much quicker" even when the underlying data requirements were unchanged.

Research directly shaped the final design. Three meaningful changes came out of testing that made the journey clearer and more trustworthy for business customers.

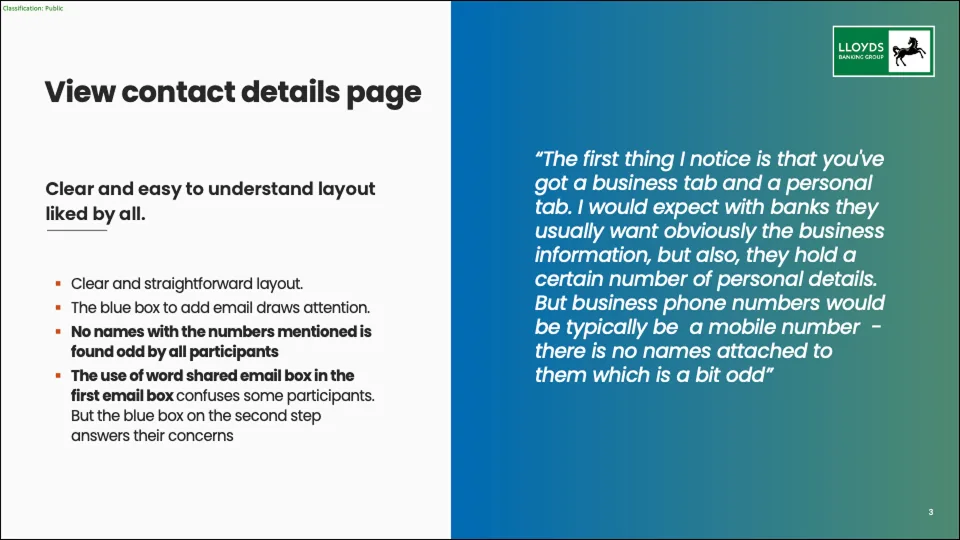

Research showed that business customers drew a clear distinction between their business contact details and their personal information. In response, the personal details section was moved out of this journey entirely and relocated to the Admin Hub section of the web platform — a more appropriate home that matched how customers mentally separated their business and personal data.

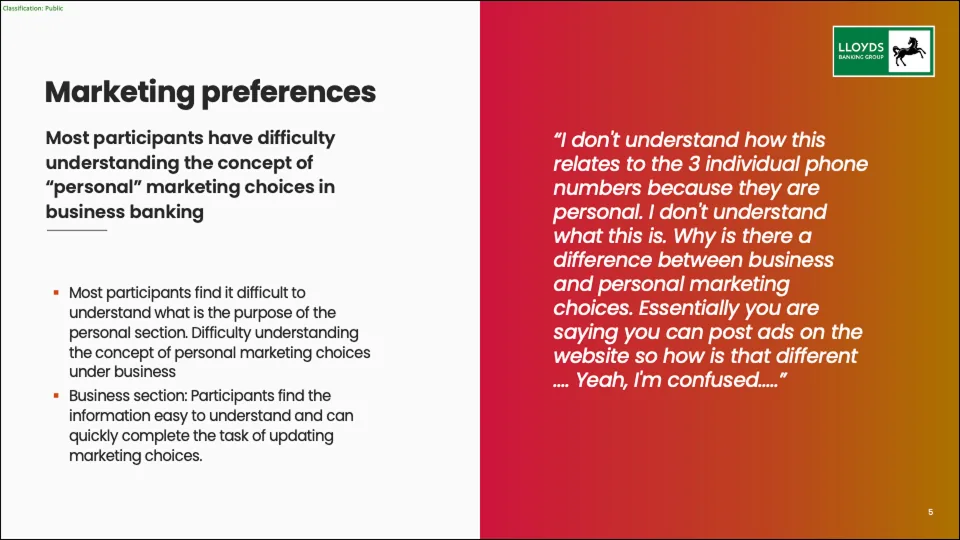

The term "personal marketing choices" was causing confusion — customers read "personal" as relating to their personal life, not their business. We rewrote the content to make clear that these were marketing preferences personalised to their business — relevant offers, products, and communications tailored to their business needs, not individual consumer marketing.

Many business banking customers also hold personal products with Lloyds. Research revealed that conflating business and personal marketing preferences in a single consent screen created distrust — customers weren't sure what they were agreeing to or for which relationship. We separated the two into distinct consent steps, each with clear context, giving customers full transparency and control over both their business and personal marketing choices independently.

Full prototype available

The complete journey is available as a password-protected file. If you'd like to see the full set of screens, get in touch and I'll provide the access details.

Total journey views from launch through end of 2025 — demonstrating strong adoption from day one.

New email addresses collected from business customers who had no email on record with the bank.

New phone numbers added — directly improving the bank's ability to reach customers for fraud alerts and communications.

Customers correcting existing email salutations — reducing the volume of impersonal or incorrectly addressed correspondence.

Of all journeys resulted in a new or updated email address or phone number — a significant improvement to data quality across the portfolio.

Journey views in the first quarter of 2026 alone — showing sustained and growing engagement.

New email addresses collected in Q1 — continuing to close the data gap at pace.

New phone numbers added in the first three months of 2026.

Customers updating their salutation preferences in Q1 alone.

Of Q1 journeys resulted in a meaningful data update — up from 64.86% at launch, showing the journey continues to improve in effectiveness.