Product OwnerStakeholder & scope

CJMCustomer journey manager

Engineering3 engineers — front & back end

QA2 testers

ResearchUser researcher

DesignUX / UI / Service designer

ContentContent writer

ExternalLegal & fraud — as needed

01

Stakeholder mapping Every project starts with a stakeholder map — identifying all team members, external colleagues, and dependencies so nothing is missed and the right people are involved from the start.

02

Working groups & requirements We ran working group sessions to align on what the project was about, documented all requirements in Jira, and looped in legal and fraud where there was a regulatory or security dimension.

03

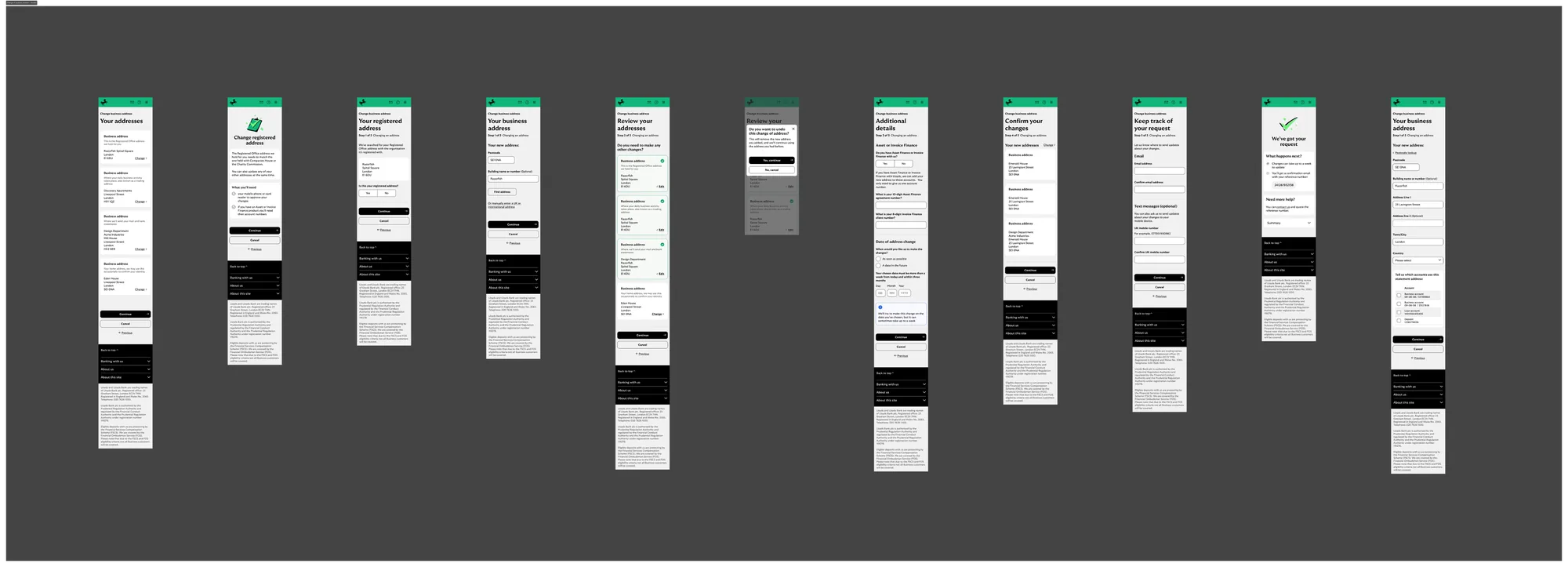

Sketches & early wireframes Before committing to any direction, I sketched ideas quickly to bring to working groups — lightweight enough to invite challenge, clear enough to spark a useful conversation with stakeholders.

04

Strawman prototype Once alignment was reached on direction, we built a strawman prototype to give the project shape — enough to stress-test assumptions internally before going anywhere near users.

05

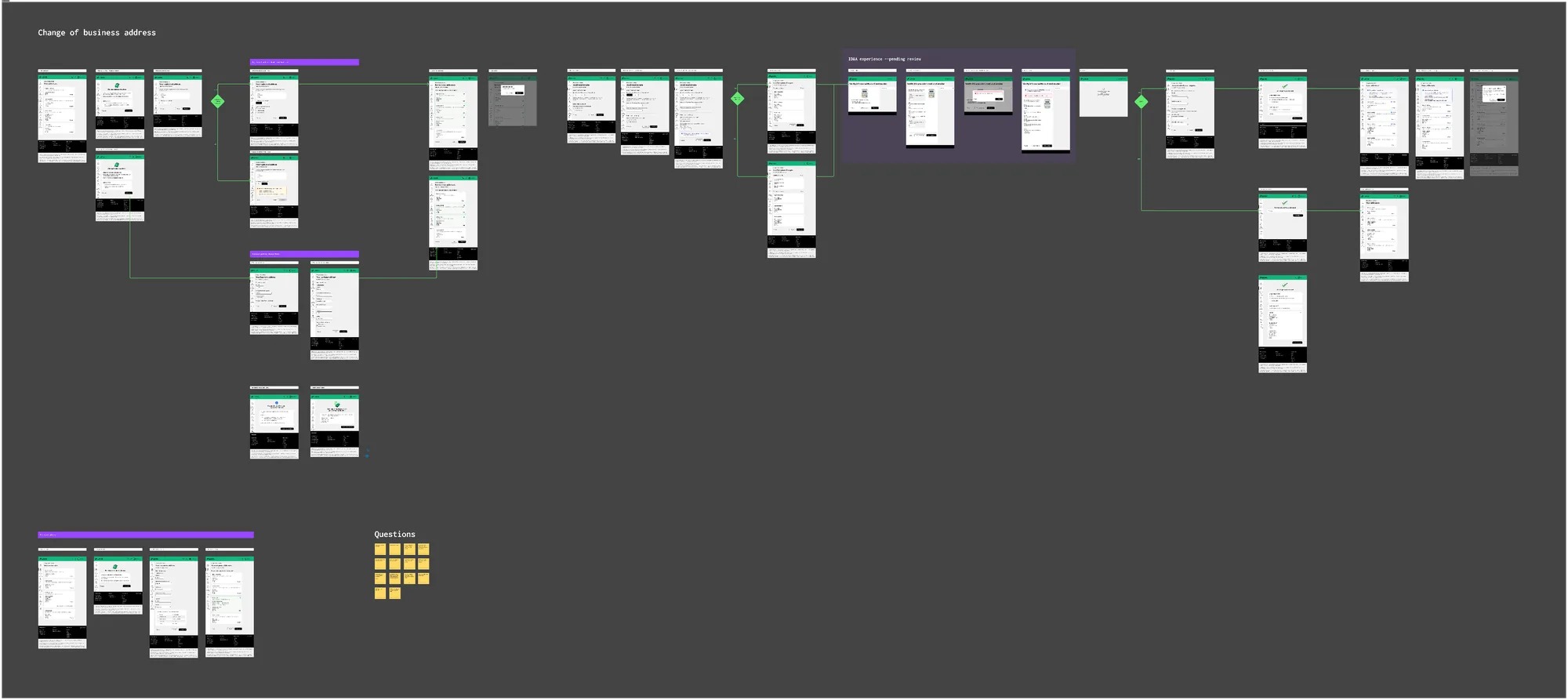

Research & iteration With something concrete to test, we created a research discussion plan and defined the assumptions we needed to validate. Testing findings fed directly back into the design — iterating until we had something we were confident to ship.

06

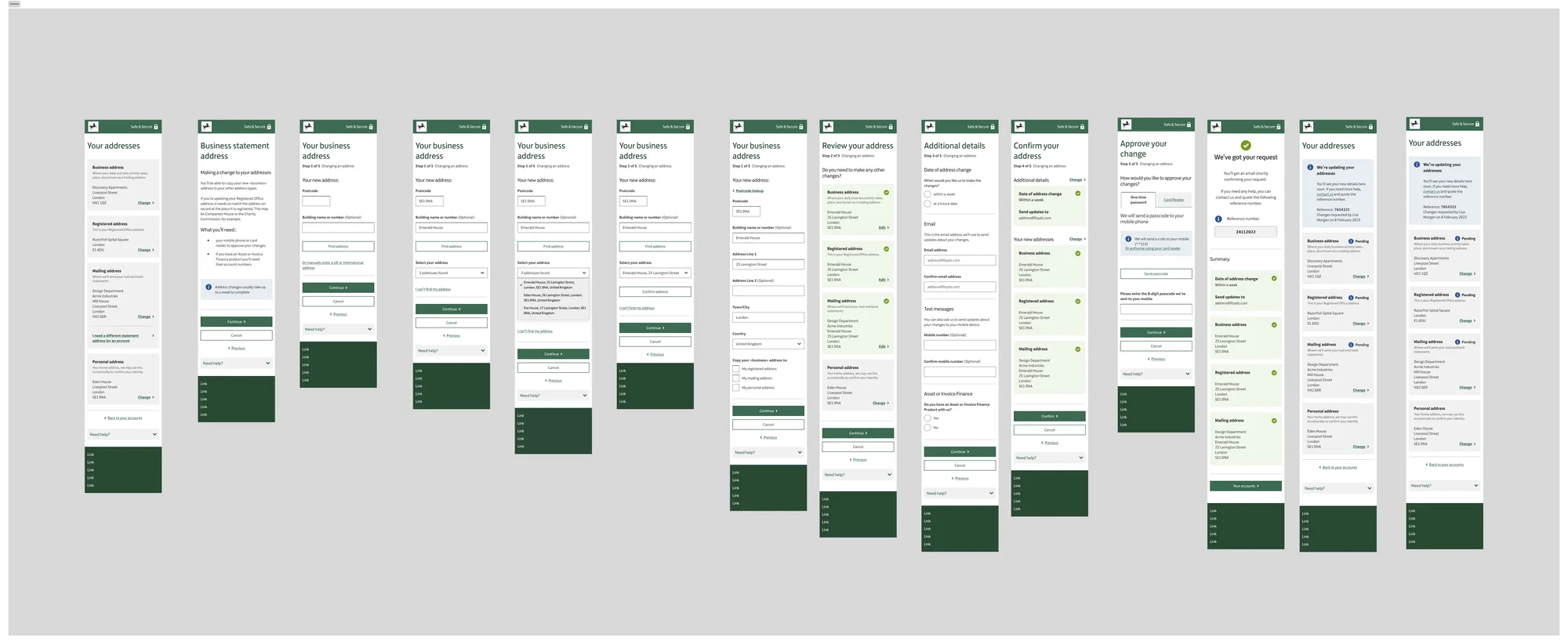

High-fidelity prototype & stakeholder sign-off Once the design was validated through research, we moved to a high-fidelity prototype reflecting the final UI and content. This was presented to stakeholders for formal sign-off — ensuring everyone from product to legal was aligned before a single line of production code was written.

07

Dev handover & build monitoring Designs were handed over to engineering with annotated specs and a dedicated handover session to walk through edge cases, states, and interactions. Throughout the build phase, I stayed close — reviewing implementations, flagging deviations, and making sure what shipped matched what was designed.

08

Performance monitoring via Power BI Post-launch, we tracked how the service was performing against the success metrics defined at the outset — adoption rate, support call volume, and data accuracy. Power BI dashboards gave us a live view of the numbers, letting us confirm we had hit our targets and identify anything that needed a follow-up iteration.